The Bank of Japan surprised investors with an unexpected change in one of the basic tenets of its monetary policy, sending shockwaves through the currency, bond and stock markets.

Traders described the adjustment to long-running yield curve control measures as potentially signaling a “pivot point” by the Bank of Japan, the last of the world’s leading central banks to commit to Very loose system.

“We consider this decision a big surprise, as we expected that the acceptable range under the new leadership of the Bank of Japan will be expanded from the spring of next year, similar to the market,” said Naohiko Baba, chief economist for Japan at Goldman Sachs.

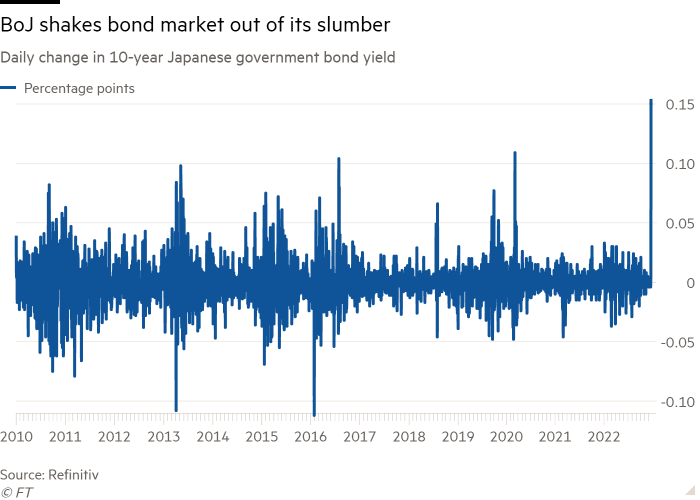

The yen jumped more than 4 percent to about 131.2 yen against the US dollar in New York trading, while the Japanese Topix index fell by 1.5 percent. The 10-year Japanese government bond yield rose to its highest level in nearly two decades, at 0.47 percent.

The Bank of Japan’s move on Tuesday also rebounded in other large markets: the 10-year US Treasury yield rose 0.11 percentage point to 3.69 per cent, while the equivalent British bond yield rose by a similar margin to 3.6 per cent. Yields go up when prices go down.

BoJ Governor Haruhiko Kuroda denied that the latest revision represented a tightening of monetary policy, stressing that the central bank would not abandon its yield target.

Japan’s increasingly extreme position contributed to a A significant drop in the yen This year the markets priced in the difference with the US Federal Reserve tightening interest rates.

The central bank said it would allow 10-year bond yields to fluctuate by 0.5 percentage points plus or minus from its target of zero, instead of the previous range of plus or minus 0.25 percentage points. It kept the overnight interest rate at minus 0.1 percent.

Kuroda had said earlier that any adjustment to the yield curve control policy would effectively amount to an interest rate hike. But he said on Tuesday that the amendment was aimed at addressing increased volatility in global financial markets and improving the performance of the bond market to “enhance the sustainability of monetary easing”.

“This measure is not a rate hike,” Kuroda said. “The YCC adjustment does not indicate the end of the YCC or an exit strategy.”

Japan’s core inflation – which excludes volatile food prices – has surpassed the Bank of Japan’s 2 percent target for the seventh straight month, hitting a 40-year high of 3.6 percent in October.

But Kuroda has long argued that any tightening would be premature without strong wage growth, which is why most economists expected the Bank of Japan to continue on course until it steps down in April. On Tuesday, the central bank maintained its forecast that inflation will slow next year and warned of “extremely high uncertainty” for the economy.

“It may be a generous act by Kuroda to ease the burden on the incoming BoJ governor, but it is a dangerous move and market players feel cheated,” said Masamichi Adachi, chief Japan economist at UBS. “US yields are now falling but if they start to rise again, the Bank of Japan will again face the risk of being pressured to raise interest rates.”

The Bank of Japan’s efforts to defend its YCC targets have contributed to a persistent decline in market liquidity and what some analysts have described as “dysfunction” in the market. Japanese government bonds market. The central bank now owns more than half of the bonds outstanding, compared to 11.5 percent when Kuroda became governor in March 2013.

Kyohei Morita, chief Japanese economist at Nomura Securities, said the BoJ’s move was probably seen as a policy adjustment rather than a complete pivot. “The BoJ may want to contribute to minimizing the negative side effects of yield curve control,” he said, noting that the bank’s massive ownership of the Japanese government bond market means that liquidity has evaporated.

“They want to reactivate that market, even as the yen goes up,” Morita said.

Mansoor Mohiuddin, chief economist at the Bank of Singapore, said the BoJ’s move was significant because it indicates the central bank is considering a broader exit from the YCC, adding that it would be an important turning point for the yen.

“The Bank of Japan’s decision to raise interest rates in December 1989 led to a major drastic change in the Japanese markets,” Mohieldin said. Those in charge today will be well aware of this history. It amplifies the importance of their signals to the markets today.”

The BoJ’s move will lead the market to start pricing in other policy moves, even if none is imminent, said Benjamin Chatel, foreign exchange strategist at JPMorgan.

“Unapologetic reader. Social media maven. Beer lover. Food fanatic. Zombie advocate. Bacon aficionado. Web practitioner.”

/cdn.vox-cdn.com/uploads/chorus_asset/file/25546355/intel_13900k_tomwarren__2_.jpg "There is no solution to the problem of Intel 13th and 14th Gen processors crashing — no permanent damage")

More Stories

Kamala Harris likely to share her stance on Bitcoin in coming weeks – industry optimists note her husband is a ‘crypto guy’

Elon Musk: Trump Presidency Could Hurt Tesla’s Competitors

GM’s very strong quarter was overshadowed by potential industry headwinds